WEAKER demand across a number of national markets and lower raw material inflationary pressures were the two main factors slowing value growth in Europe’s flexible packaging market in 2012, according to market intelligence provider PCI Films Consulting.

In 2012 annual value growth in flexible packaging slowed to 2.1%, down from over 5% in 2011. Weaker demand from flexible packaging buyers as they responded to static sales of packaged food by reducing stock levels was one contributory factor. Another was that in 2012 the industry was able to avoid a repeat of the inflationary pressures experienced in 2011 when the cost of plastic films, foils and papers, inks and adhesives rose significantly and in order to maintain margins converters had to pass these increases on to customers.

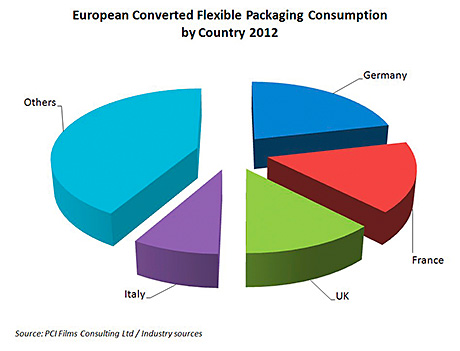

These are some of the main conclusions from PCI’s latest annual report on the €12.1 billion European converted flexible packaging market, and a similar picture of a modest increase is expected to emerge for 2013. Report author Paul Gaster notes, “While value growth has slowed, European consumption of flexible packaging in volume terms approached 2% in 2012, confirming that flexible packaging continues to perform better than many other industries in the current economic climate”.

The report details some significant regional and national differences in demand trends. While there was modest expansion in Europe’s largest market, Germany, little or no growth was seen in the UK and France and there were real declines across Southern Europe in Italy, Spain, Greece and Portugal, as these economies continued to struggle. The standout markets again this year were Turkey, and key East European countries, Russia and Poland, which increased in value at more than twice the European average.

20% of the flexible packaging industry’s sales in Europe are currently generated by private equity portfolio companies

Consolidation continues to be another important factor changing the structure of the industry with Mondi Packaging’s acquisition of Nordenia International and the enlargement of Schur Flexible via a series of medium sized acquisitions, being significant developments last year. As in past years, private equity firms played a prominent role in flexible packaging and one firm, Sun Capital, has made a series of acquisitions in Europe and North America to form Exopack Holdings. This company is now ranked amongst the top 10 players in Europe. Mr Gaster notes that, “20% of the flexible packaging industry’s sales in Europe are currently generated by private equity portfolio companies”.

{kind=link}